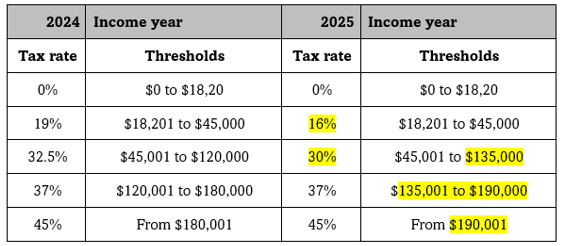

BUSINESSES

$325 energy rebate

Similar to the household rebate, small businesses will receive $325 off the next year’s electricity bills. A qualifying small business will be one that:-

- Has a turnover (gross income) of less than $10,000,000 (but it is unclear how an electricity company will know whether to apply the grant or not) and

- Have annual electrical consumption under 40 MWh. It is unclear why small businesses with greater consumption (manufacturers and the like) won’t receive a benefit.

$20,000 asset write-off

The $20,000 asset write-off will be extended for another 12 months from 1st July 2024 for small businesses with turnover under $10,000,000.

That said, the bill to extend the $20,000 write-off for this financial year ending 30th June 2024 has yet to be passed. As annoying as that is, it must also be said there are two proposed amendments – to increase that limit to $30,000 for this 2023/24 year and be extended to businesses with annual group turnover under $50,000,000.

TIP The $20,000 is the ex GST amount.

TRAP An asset costing more than $20,000 is subject to depreciation under the Simplified Tax System – 15% in the year of acquisition followed by 30% of the remaining balance in following years.

TIP If you are thinking of buying a $40,000 asset you need for your business and the price is good, buy it before July – that way your business can claim 15% in this tax year (even though owned for a few weeks) and the 30% of the residual 85%. So your business is able to claim $16,200 of depreciation in the first 54 weeks of ownership – but only $6,000 if bought in the first week of July.

TIP The asset must be installed ready for use by 30th June 2024.

TIP There is no grouping of like items – your business could claim the cost of 30 lap-tops costing $1,500 each.

TRAP The write-off threshold is set to return to $1,000 from 1st July 2025 – but history has shown that both left and right wing governments love to extend it.

Retaining BAS refunds

The period in which the ATO can retain a BAS refund will be increased from 14 to 30 days. As unwelcome as that sounds, the reality is that it gives the ATO a better opportunity to detect fraud (and therefore protect the public purse).

Building cyber resilience for small business

I remain sceptical about the millions spent within Canberra on committees and reviews staffed by bureaucrats without any real input sought from industry bodies and small businesses. But it is pleasing to see 3 announcements in respect of cyber protection:-

- Cyber wardens to provide free on-line training.

- The introduction of a Small Business Cyber Resilience Service to both help small businesses build their cyber resilience and moreover provide support in response to a cyber incident.

- The introduction of an online Cyber Health Check so small businesses can self assess their situation and exposure.

TIP Upcoming government support should not let you decide to deal with this later. And in particular, seriously consider adding cyber insurance cover to your existing business policy(ies).

TIP The best policy is not the cheapest; the best policy is the one that will cover you for what you need when you need it.

Unpaid super entitlements on liquidation

Currently employee’s pay and leave entitlements are protected under a federal scheme. That scheme however doesn’t extend to unpaid superannuation. From 1st July 2024, directors of companies which have entered liquidation can be pursued for unpaid super.

ATO will cease chasing old tax debts

Out of the blue, the ATO started chasing old tax debts they had previously written off; debts that had long since been forgotten and did not show in either Tax Agent Portal or Taxpayer Portal. Tax debts that had been “put on hold” before 1st January 2017 can no longer have a tax refund offset against those debts. |